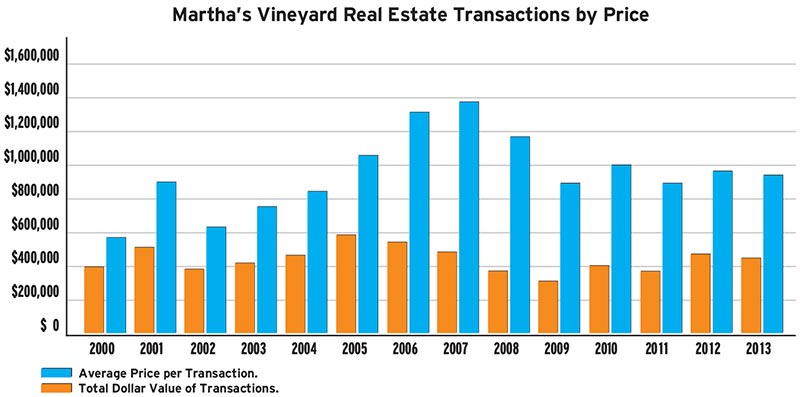

The Martha’s Vineyard real estate market improved in 2013, but the advance over the year before was modest, and early signals from sales statistics for the first half of 2014 suggest that growth continues to be variable across market segments, leaving prospects for the rest of 2014 uncertain. A compilation of market statistics from LINK data, as well as data from MVTimes records and observations from brokers, all shown plainly in the accompanying graphs, make clear that the market collapse after 2007 led relentlessly to fewer annual sales and a collapse in for-sale inventories. The market found a bottom in 2009-2010 and has continued to potter along there since.

{kind=link}

The stand still nature of market progress over time become is clear when one compares total sales in 2003, 566, with total sales last year, 502. That’s an 11 percent decline over the decade. Then, looking at the numbers comparing total sales for 2008, 314, and last year, 502, the change over six years was slightly greater than 60 percent. Together the two comparisons describe the steep and deep nature of the financial collapse, now familiarly known as the Great Recession, and the incomplete nature of the recovery.

At the same time, and to some degree mirroring the way the recovery has generously benefited the financial economy but been more niggardly about helping the real economy, one finds that the share of sales of property worth more than $1 million rose sharply between 2008, 87, and 2013, 144, although for property sold for more than $3 million, the difference between 2008 and 2013 has been negligible, 24 six years ago, 22 last year.

{kind=link}

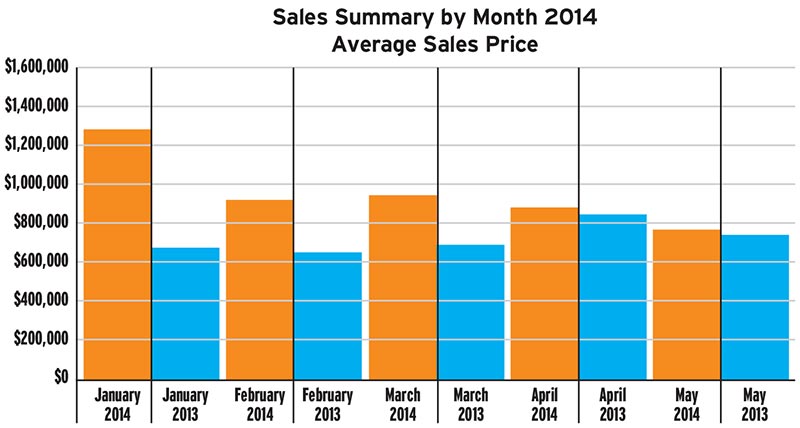

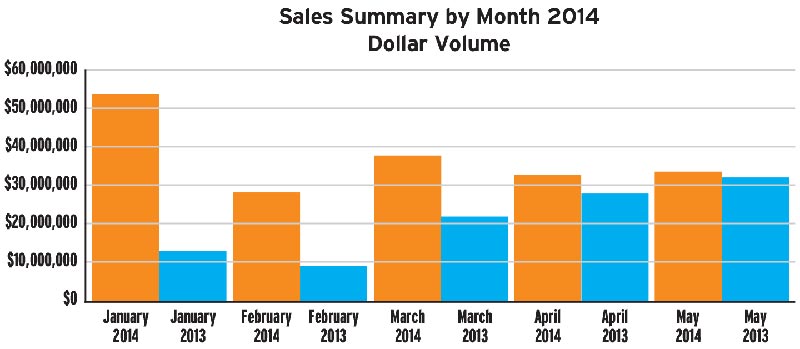

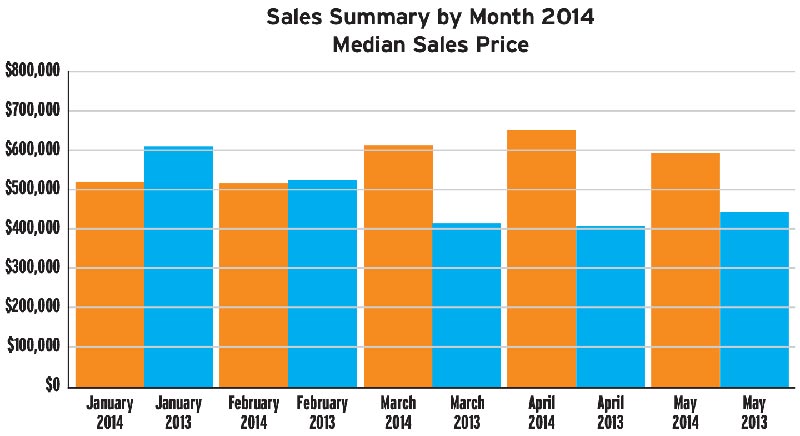

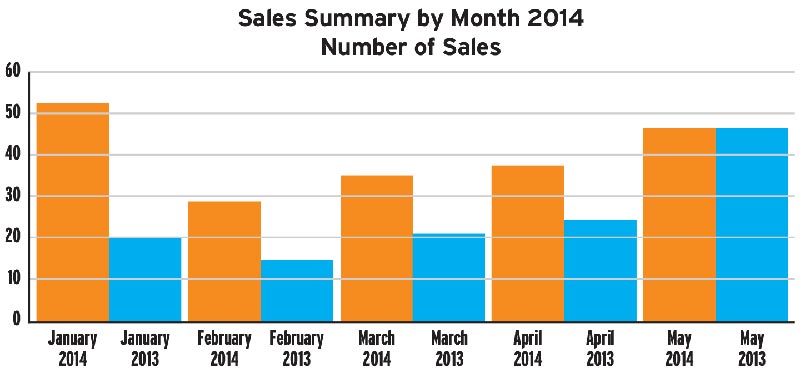

What the results for the first five months of 2014, compared with the first five months of 2013 show is that the year-over-year margins in these measures have narrowed, and the overall strength of the market last year has diminished in the first half of this year. In January 2014, 52 sales were recorded as against 20 in January last year. In May this year there were 46 completed transactions, exactly as many as were recorded in May 2013. In January this year, $54 million in sales took place as against $14 million in January last year, but in May, the year-to-year dollar comparison for the month found that $35 million in property changed hands in January this year, compared with $33 million in the same month a year ago. In January this year, the average sales price was $1 million, compared with just $676,000 in January a year ago. In May 2014, the average price was $759,000, compared with $724,000 in May 2013.

Interestingly, the share of total sales represented by transactions worth less than $1 million has declined over the decade since 2003, suggesting that the resources of buyers, as well as the sellers’ conclusions about the value of their properties, have increased. In 2003, when 566 transactions took place, 83 percent of those deals were for properties sold for less than $1 million. In 2008, the under-$1 million share was 72 percent, and in 2013 it was 71 percent.

In general terms, real estate insiders mostly call the 2013 performance of the market flat.

{kind=link}

The change in the inventory of property for sale flattened in 2013. Sales are little changed compared to sales in 2012. The dollar value of property sold in 2013 is barely greater than in 2012. The average value of sales didn’t change materially either. The Vineyard market may have held up better in the immediate aftermath of the 2007-2008 collapse and may have been slower to reach the bottom. Also, the bottom here has not been as catastrophic here as it has been in some other U.S. markets. But, the Vineyard market has not resumed its historically buoyant ways. Brokers say that buyers are plentiful and eager, but nervous about the country’s economic future, and they want their ideal vacation properties at ideally low prices. Inventories, historically high before the recession, declined rapidly as prices fell and buyers disappeared, but they have risen slowly as sellers return to what they see as a strengthening market.

The Chilmark market, historically characterized by high prices and low volume, has seen sales volume decline, along with prices. Chilmark recorded only 32 sales last year, 40 percent fewer than in 2012. The number of transactions recorded in Chilmark has historically been small, but the town has regularly been second only to Edgartown in dollar value of sales. In 2013, the value of its 32 sales dropped 50 percent compared with the year earlier results, to just $11 million.

{kind=link}

In wealthy, diverse Edgartown, 2013 results contrasted sharply with those of the small, rich up-Island town. Edgartown, vast geographically and its inventory spanning all market pricing segments, saw 2013 sales volume jump 15 percent compared with 2012. Dollar value for all sales rose 10 percent. In 2013, $233 million in real estate changed hands, compared with $40 million in Chilmark.

West Tisbury, $56 million, and Oak Bluffs, $59 million, saw total value of sales drop in 2013, compared with the year before. Tisbury recorded an astonishing 40 percent jump in the total value of sales, to $84 million, year over year.

{kind=link}